When analyzing a potential rental property investment, the numbers need to work. You calculate expected rental income, estimate operating expenses, and project cash flow—but there’s one variable that can make or break the deal: your interest rate. Even a difference of 0.5% on a £300,000 DSCR loan translates to thousands in additional costs over the loan term.

DSCR loan interest rates operate differently from standard mortgage rates. They’re typically higher, structured differently, and influenced by factors beyond just your credit score. Understanding what drives these rates—and what you can control to improve your pricing—is essential for making smart investment decisions.

This guide explains how DSCR loan interest rates are determined, why they’re often priced above conventional mortgages, and practical strategies to secure more competitive terms.

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Today's Mortgage RatesMcGowan Mortgages specializes in comparing DSCR loan options from multiple lenders, helping investors understand their rate options and negotiate favorable terms.

What Are DSCR Loan Interest Rates?

DSCR loan interest rates are the rates charged on mortgages underwritten primarily based on Debt Service Coverage Ratio—the property’s ability to generate sufficient rental income to cover its mortgage payments—rather than the borrower’s personal income documentation.

These loans are specifically designed for investment properties: rental homes, multifamily buildings, commercial properties, and mixed-use assets. Because they serve a different purpose and carry a different risk profile than owner-occupied mortgages, DSCR loan interest rates are typically priced higher than rates advertised for primary residence mortgages.

The premium reflects several factors including the specialized nature of these products, the focus on property cash flow rather than personal income, and the fact that investment properties historically experience higher default rates. While exact rates vary significantly based on individual circumstances, DSCR loan rates generally run 0.5% to 1.5% above the best conventional owner-occupied mortgage rates.

Are DSCR Loan Rates Fixed or Variable?

One of the first decisions you’ll face is choosing between fixed and variable rate structures.

Fixed-rate DSCR loans lock in your interest rate for the entire loan term—commonly 15, 20, or 30 years. Your monthly payment remains constant, making cash flow projections straightforward and protecting you from interest rate increases. Fixed rates provide certainty that’s particularly valuable for buy-and-hold investors focused on long-term rental income.

The trade-off is that fixed-rate DSCR loans typically start with slightly higher rates than adjustable-rate options.

Adjustable-rate DSCR loans (often structured as 5/1, 7/1, or 10/1 ARMs) start with a fixed rate for an initial period, then adjust periodically based on a market index. These products often offer lower starting rates, which can improve initial cash flow and returns. If you plan to sell or refinance within the initial fixed period, you might benefit from the lower starting rate without experiencing rate adjustments.

However, adjustable rates carry interest rate risk. Once the adjustment period begins, your rate and monthly payment can increase if market rates have risen.

Which should you choose? Choose fixed rates if you’re planning to hold the property long-term (10+ years), want maximum payment predictability, or believe interest rates are likely to rise. Consider adjustable rates if you plan to sell or refinance within 5-7 years, want to maximize initial cash flow, or are comfortable managing interest rate risk.

Why Are DSCR Loan Interest Rates Often Higher?

Understanding why DSCR loan rates carry premiums helps contextualize your options and manage expectations.

Cash flow underwriting creates different risk. Traditional mortgages verify your personal income extensively to ensure you can afford payments regardless of property performance. DSCR loans rely primarily on the property’s rental income, which lenders view as less stable. Rental markets fluctuate, vacancies occur, and expenses can spike unexpectedly. This perceived additional risk translates to higher rates.

Specialist and non-bank lenders. Many DSCR loans come from specialist lenders or non-bank financial institutions rather than major banks. These lenders often have higher funding costs, which they pass to borrowers through higher rates. The trade-off is more flexible underwriting and willingness to finance situations traditional banks decline.

Investment property risk premium. Investment properties statistically default at higher rates than owner-occupied homes. When financial pressure hits, borrowers prioritize keeping their primary residence over investment properties. Lenders price this risk into rates.

Portfolio and complex properties. DSCR loans often finance larger amounts, multiple properties, or complex assets like multifamily buildings. These situations require more sophisticated underwriting and create different risk profiles, contributing to rate premiums.

While DSCR loan rates run higher than owner-occupied mortgages, they’re often competitive with other investment property loan options like portfolio loans or commercial mortgages.

How Do Lenders Calculate DSCR Loan Rates?

DSCR loan interest rates aren’t arbitrary—lenders use systematic approaches to assess risk and price loans accordingly.

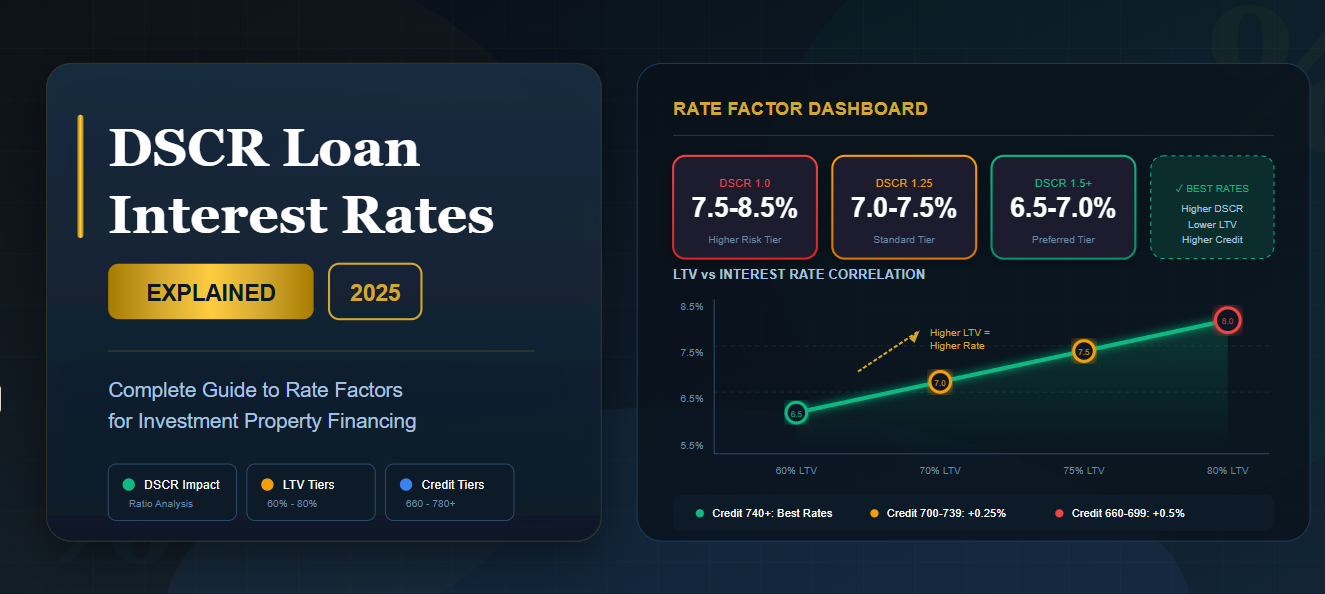

Your DSCR level is the primary driver. Higher DSCR signals stronger cash flow and lower risk, potentially qualifying you for better pricing. A property with DSCR of 1.4 demonstrates robust income generation, likely receiving better rates than a property barely meeting the 1.0 minimum threshold. Many lenders have tiered pricing structures where even modest DSCR improvements can move you into better pricing tiers.

Loan-to-Value ratio significantly impacts rates. Lower LTV means more equity cushion, reducing lender risk. Many lenders offer their best rates at 70-75% LTV, with pricing becoming progressively less favorable as LTV increases toward 80-85%.

Borrower credit profile and experience matter significantly. Borrowers with scores above 740 typically access the best pricing, while those below 680 may face rate premiums of 0.5-1.0% or more. Your track record as an investor—demonstrated success managing rental properties, stable occupancy, timely payments—also influences rates.

Property type and location affect pricing substantially. Single-family rentals in strong, stable rental markets typically qualify for the best rates. Small multifamily properties often receive similar treatment. Larger multifamily, mixed-use buildings, or properties in weaker rental markets may face higher rates. Location matters—properties in markets with strong rental demand, low vacancy rates, and stable values receive better pricing.

Loan structure and size influence rates. Interest-only loans often carry rate premiums compared to amortizing loans. Longer fixed-rate periods typically come with higher rates. Very small loans may face rate premiums, while very large loans may receive preferential pricing.

Market conditions and volatility affect DSCR loans. They’re influenced by broader mortgage rate trends, central bank policy rates, inflation expectations, and overall credit market conditions. During periods of market stress, DSCR loan rates may become less competitive.

Factors Investors Can Control to Get Lower DSCR Loan Rates

While you can’t control market rates, you can influence several factors affecting your personal rate offer.

Improve your DSCR and cash flow. If your property is under-rented relative to market rates, bringing rents up improves DSCR and can move you into better pricing tiers. Reducing operating expenses—negotiating better insurance rates, optimizing maintenance spending—improves net operating income and DSCR.

Reduce LTV where possible. If you can afford a larger down payment, reducing LTV often unlocks better rates. Many investors find that interest savings from moving from 80% to 75% or 70% LTV justify the additional capital commitment.

Strengthen your credit and track record. Improving your credit score takes time but pays dividends. Pay down credit card balances, ensure on-time payments, and avoid new credit inquiries before applying. Document your success as an investor with financial statements showing stable property performance and strong occupancy.

Choose your loan structure strategically. A 20-year fixed rate typically carries lower rates than a 30-year. If you’re confident about refinancing within 5-7 years, adjustable-rate products with lower initial rates can reduce your effective borrowing cost.

Work with a specialist broker. McGowan Mortgages maintains relationships with multiple DSCR lenders, understands their current pricing grids, and knows which lenders are most likely to offer competitive rates for your specific situation. Brokers can often negotiate better terms because they represent volume to lenders.

Can you negotiate a lower DSCR loan rate? Yes, often—through demonstrating strong deal fundamentals, working with a broker who has lender relationships and negotiating leverage, and presenting yourself as a desirable borrower.

DSCR Loan Interest Rates by Property Type

While individual circumstances vary, general patterns exist in how different property types are priced.

Single-family rentals in strong markets typically receive the most competitive DSCR loan rates. These properties are most similar to conventional real estate lenders understand well, have good liquidity, and demonstrate predictable performance.

Small multifamily (2-4 units) often receive pricing similar to single-family rentals, sometimes even better. Lenders appreciate the diversified income stream—one vacancy doesn’t eliminate all rental income.

Larger multifamily (5+ units) enter commercial real estate territory, requiring more sophisticated underwriting. Pricing varies more widely depending on property quality, location, and management. Strong properties can still secure reasonable rates through specialized lenders.

Mixed-use and commercial properties often face higher rates or stricter DSCR requirements due to added complexity and potential income volatility. Strong properties in excellent locations with stable commercial tenants can still secure reasonable rates.

Specialized properties like short-term rentals or vacation properties may face rate premiums reflecting their specialization. Income from platforms like Airbnb is viewed as less stable, leading to higher rates or minimum DSCR requirements of 1.3-1.5.

When Do DSCR Loan Interest Rates Still Make Sense?

Even with rate premiums, DSCR loans often represent the best financing choice when you evaluate the complete picture.

DSCR loans make strategic sense when they enable portfolio growth beyond what conventional lending allows. If traditional lenders have capped you at 4-10 properties but you have opportunities to acquire additional cash-flowing properties, paying a rate premium to continue growing often produces better long-term returns.

They make sense when income documentation creates barriers. If you’re self-employed with complex income, DSCR loans may be your only viable financing option. They make sense for properties where strong cash flow justifies the rate—if your property generates DSCR of 1.4+ with excellent rental income, it easily supports the slightly higher payment.

Consider the complete investment picture: calculate your net cash flow after mortgage payments, factor in tax benefits, and project your total return on equity over your expected hold period. Often, the rate difference matters less than factors like portfolio growth, convenience, and strategic positioning.

How McGowan Mortgages Helps You Find Competitive DSCR Loan Rates

McGowan Mortgages specializes in investment property financing and maintains active relationships with multiple DSCR lenders. They understand each lender’s current pricing, appetites, and specializations, knowing which are most competitive for different property types and borrower profiles.

They can review your property’s DSCR, analyze your borrower profile, and identify opportunities to strengthen your application before submitting to lenders. They’ll present actual rate options from multiple lenders, allowing you to compare complete loan packages including fees, terms, and flexibility.

Explore the learning center for more insights on investment property financing strategies.

Frequently Asked Questions About DSCR Loan Interest Rates

Are DSCR loan interest rates always higher than regular mortgage rates?

DSCR loan rates are typically 0.5-1.5% higher than owner-occupied mortgage rates, but not necessarily higher than other investment property financing options. They’re often competitive with portfolio loans and commercial mortgages. Compare conventional investment property loan options to understand the full landscape.

What factors have the biggest impact on the DSCR rate I’m offered?

Your property’s DSCR level, loan-to-value ratio, credit score, and property type/location are the primary drivers. Properties with DSCR above 1.25, LTV below 75%, credit scores above 720, and strong locations receive the best pricing. Check current mortgage rate trends to understand market conditions.

Should I choose a fixed or adjustable DSCR loan rate for my rental property?

Choose fixed rates if you’re holding long-term (10+ years) and want payment certainty. Consider adjustable rates if you plan to sell or refinance within the initial fixed period (typically 5-7 years) and want lower starting rates. Your risk tolerance and market rate outlook should guide this decision.

Can I refinance a DSCR loan later if interest rates fall or my DSCR improves?

Yes, you can refinance DSCR loans, though watch for prepayment penalties. If market rates fall significantly or your property’s DSCR improves substantially, refinancing can reduce your rate and improve cash flow. You might also consider HELOCs or home equity loans for accessing equity.

How can a broker like McGowan Mortgages help me secure a lower DSCR loan interest rate?

McGowan Mortgages accesses multiple DSCR lenders simultaneously, knows which offer the most competitive rates for your property type, can identify opportunities to strengthen your application, and often has negotiating leverage that individual borrowers lack. Contact them to discuss your situation, or check the FAQs for more guidance.

Ready to explore DSCR loan rates for your investment property? Contact McGowan Mortgages today to discuss your property, review your options, and find competitive financing. Our team specializes in DSCR loans and investment property financing, helping investors secure favorable terms that support their portfolio growth.

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Today's Mortgage Rates