Big news out of Jackson Hole this past week! Federal Reserve Chair Jerome Powell suggested that the labor market may be taking priority over inflation for now. The markets took that as a green light — and mortgage rates have dropped to fresh 2025 lows.

👉 The average 30-year fixed Conventional rate is now 6.52% — the lowest we’ve seen this year.

(This is assuming the ‘perfect situation’ – Purchase, 20% down, 800+ credit, low Debt-to-Income Ratio, Single-Family Home, etc.)

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Today's Mortgage RatesWhy This Matters for Buyers & Agents

When rates move from the mid-6’s toward 6%, we usually see housing activity pick up.

Recent data shows 29 straight weeks of positive year-over-year purchase applications.

For the past 16 weeks, growth has been in the double digits compared to last year.

The last 3 weeks of rate stability under 6.64% have already translated to more buyers stepping into the market.

If rates can dip closer to 6% and stay there, history tells us we could see a nice run of 12–16 weeks of stronger housing demand — which means more homes going under contract.

What’s Next?

The rest of the year will be shaped by:

- Federal Reserve decisions and leadership talk 🏦

- Labor market updates 👩💻

- Trade/tariff news 🌎

- General election-year speculation 🗳️

All of this could impact how long rates hold near these lows.

Bottom Line

This is a rare window where rates are low and home prices have softened slightly from last year’s highs. If you’ve been sitting on the sidelines, now may be the time to get Pre-Approved and get ahead of the competition.

🔑 At McGowan Mortgages, we track the market daily so you don’t have to — making sure our buyers and Realtor partners are in the best position to win.

If You Read Nothing Else, Read This

👉 The Fed may cut rates in September… but that doesn’t automatically mean mortgage rates will fall afterward. In fact, the last time the Fed cut rates (Sept 2024), mortgage rates actually moved higher within days.

Here’s What’s Happening Now:

Markets are betting on a better than 80% chance of a Fed rate cut in September.

Those odds jumped after Fed Chair Jerome Powell’s speech at the annual Jackson Hole Symposium, where he acknowledged signs of a softer job market.

Mortgage rates respond to expectations about future economic data—not the Fed’s actual meeting day decision.

Right now, those expectations pushed rates to their lowest point of 2025 (the lowest since October 2024).

💡 Why This Matters For Buyers & Homeowners:

Rates often improve before the Fed takes action. By the time the Fed cuts, markets may already have “priced it in.”

If economic data in the fall shows weakness, rates could hold steady or improve further. If the data flips stronger (like late 2024), rates could jump quickly.

What you should do:

Buyers: Don’t wait until September hoping for a Fed cut—today’s rates are already near the year’s lows.

Homeowners: If you’ve been considering a refinance, this may be the best window in months.

At McGowan Mortgages, we track these shifts daily so you don’t have to. Whether it’s locking in today’s low rate or setting up a strategy for the fall, we’ve got you covered ✅

Ellermania 2025 was a Success!

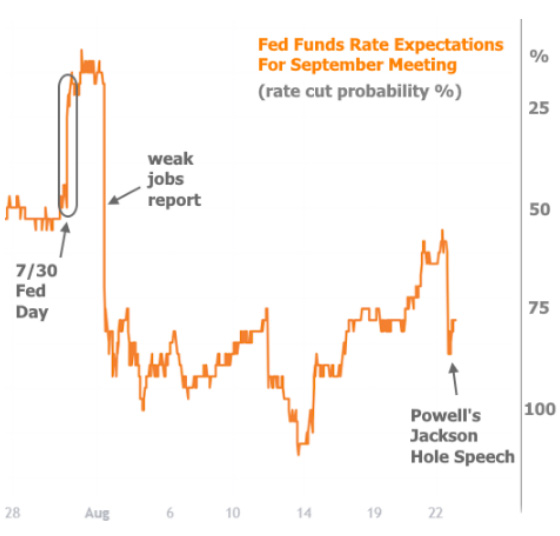

Market Odds of a Fed Rate Cut in September

You can see just how much the Fed meeting and Jerome Powell’s speech made the market move in favor of a September rate cut.

👉 Here’s the key takeaway:

The financial markets don’t wait for the Fed to actually cut rates—they react ahead of time.

Because the market is already confident a September cut is coming, mortgage rates have bounced back to the lowest levels of 2025.

That means there isn’t necessarily “more gold at the end of the rainbow” during the Fed’s September 16–17th meeting. Rates are improving now.

💡 What this means for Buyers & Realtors:

Buyers: Jumping in now means you can shop with today’s low rates before competition heats back up.

Realtors: Share with your clients that this is a rare moment—rates are as good as they’ve been in a year, and home prices haven’t yet jumped from the rush of returning buyers.

✨ Bottom line: There’s a great window of opportunity right now. Waiting could mean more buyers, more bidding wars, and higher home prices.

Interesting Developments in Housing and Mortgage Markets

📉 Mortgage rates are near their lowest since Oct 2024… and 🏡 home prices are softening?

That combo is RARE — and it could be a short window of opportunity. Here’s why 👇

Over 1/3 of the inflation report (CPI) is housing costs. As rents and prices dip, inflation cools — and that’s fuel for lower mortgage rates.

If rates drop further, expect a wave of buyers to flood back in and push prices up again.

📊 Stay ahead of the curve. DM me to game plan your next move.

🚫 Mortgage Myth Busted 🚫

“Approved for $500k? That doesn’t mean you can buy a $250k home and use the rest for upgrades. 🛠️🏠

Your loan is based on the home’s value, not a blank check. There are special renovation loans, but they come with higher rates, extra fees, and stricter rules. 📈💸

💡 Tip: If you want to roll repairs or upgrades into your mortgage, ask your lender about renovation loan options before making an offer.

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Today's Mortgage Rates