Honored to be awarded the ‘Top 40 under 40’ by National Mortgage Professional

Loan Officer/Branch Manager

McGowan Mortgages

If you could go back in time, what advice would you give your younger self starting out in the industry?

“Go for it! Get a strong foundation, including the right people around you — then don’t be afraid to dream.

My wife, Thao, does a ton to help, so I would tell my younger self to find the right partner who cares about the business, don’t take shortcuts, and you’ll be surprised where this career will take you.

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Today's Mortgage RatesIt’s tough to imagine when you’re starting out, but the sky’s the limit.

I used to tell myself that I didn’t have the most experience, but I could outwork the rest of the room. That’s the one thing that’s always an option to get ahead and help your clients — when you have the instincts always to do more for your clients and the experience comes, then watch out — because this thing will start to grow faster than you can imagine.”

How would you describe your leadership style, and how do you inspire your team?

“My leadership style has a lot of sports influences.

It resonates so much more when the coach/leader was a player themselves.

I want my team to know I’m never afraid to jump into the trenches to help.

I want to lead by example. I want the team to see me working during the day, so they know my drive to take us to higher heights.

We’re all adults, so I keep an open dialogue with the team — I let them know we’re never done growing, and I’m never set in my ways, so I encourage those who think outside the box and bring up good ideas to make us better.”

3 Reasons to Refresh your Approval!

Completely understand if financing didn’t work once, it’s not always fun to relook at things – but sometimes there can be a better answer waiting for you!

We save deals every week that didn’t qualify at other lenders.

- Not all Lenders are created equal

- Time can heal

- Get the right diagnosis

The Fed cut, but Mortgage Rates went up?!

Fed rates = short-term rates (auto loans, credit cards, etc)

Mortgage rates = long-term rates

The market also knew the Fed was going to cut. It was 96% odds, so no reaction with the Fed cutting their funds rate another .25%.

What the markets care about is what the Fed’s overall outlook on inflation and the economy is.

When the Fed said they were considering slowing down future rate cuts, compared to the initial pace they estimated, that was new info which spooked the markets.

Mortgage Rates went up on average about .2% on Wednesday alone.

The market did recover some of that on Friday when PCE Inflation came in at just 0.1% month-over-month, compared to the 0.2% projection.

The reason the Fed would slow down their upcoming rate cuts would be because they’re not as sold as they once were that inflation is under control.

We’ve spoken many times about how inflation is the driving force on where mortgage rates head next.

(see ‘Mortgage Rates and Inflation’ video)

Low inflation = low mortgage rates

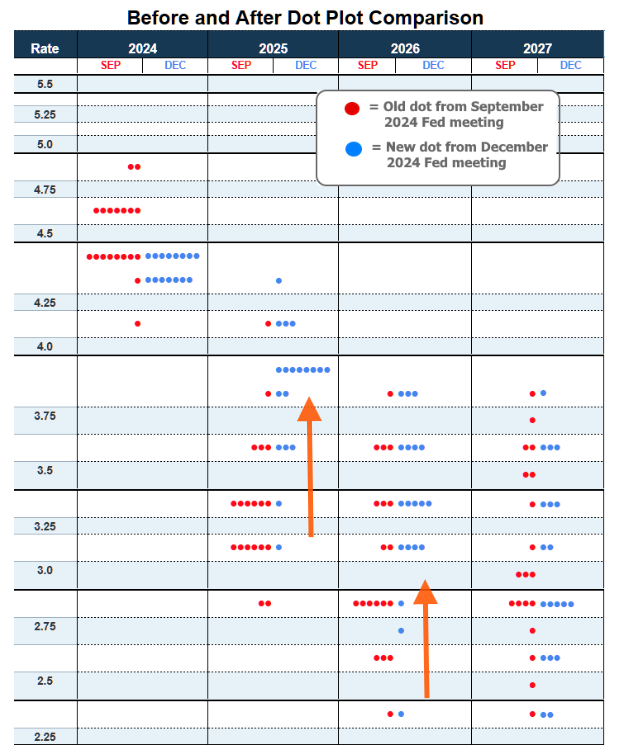

The Fed’s Dot Plot

| Below you’ll see the comparison of what the Federal Reserve members originally predicted for future Fed rates back in September – vs – what they have updated their projections to at their meeting on 12/18. You can see originally the Fed was thinking around 3.25% in 2025 and around 2.75% in 2026, but they’ve now pulled those expectations back to around 3.75% in 2025 and 3.25% in 2026. This is to ease into rate cuts to not fire inflation back up, which is a concern to mortgage rates, which was the cause for this week’s rate spike. |

Market Reaction

The moment Jerome Powell, the Fed speaker, took the stage and spoke about how the Fed feels they need to calm down on upcoming rate cuts, you can see the direct response from the market.

The chart below is 10-year Treasury, which acts as a floor for mortgage rates.

30 yr fixed Conventional mortgage rates are about 2-3% higher than the floor on average.

Do you know how much home you can afford?

Most people don’t... Find out in 10 minutes.

Today's Mortgage Rates